We Asked 676 People in the Home-Buying Market About Money; Here’s What They Told Us

Money is always a complicated subject, but perhaps most of all when you’re buying a house. A home is likely the most expensive purchase you’ll ever make, and behind that big list price is a whole micro-economy of fees, calculations, and costs that can sound downright mystifying from the outside — and inside, too!

So we asked 676 Apartment Therapy readers just like you to break down the financial aspects of their home-buying process. These are people who either recently purchased a home or are currently in the market, and their intel is part of our State of Home Buying survey, presented in partnership with Homes.com. Homes.com goes above and beyond to provide home-shoppers the most in-depth information in a beautifully streamlined design, and always connects you to the listing agent who can answer any questions you may have.

Home-buying comes with a lot of questions, especially financial ones. Consider these survey responses a map for finding your own answers.

The Down Payment

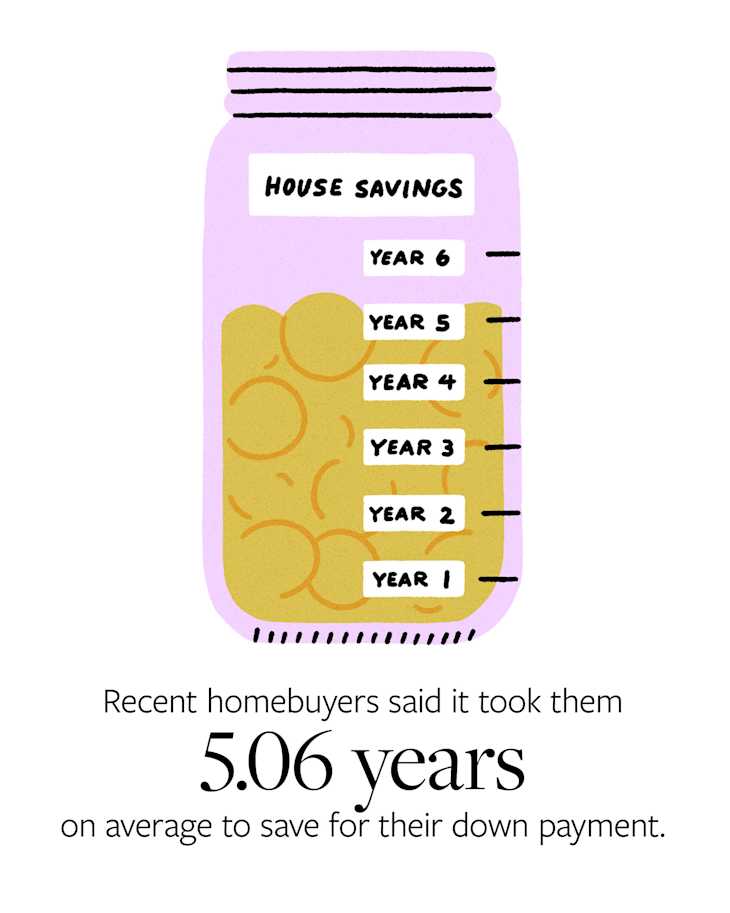

There’s no one-size-fits-all approach to down payments, but our recent homebuyers put down an average of 27 percent for their homes. Prospective buyers were looking to put down an average of 21 percent. They said it took them approximately 4.5 years to save up. With Homes.com’s in-depth neighborhood guides, you can get a clear, hyper-local picture of the market, so you can feel confident about how much you should save. Use the guide to view trends like median sale prices, year-over-year price changes, and even median discounts from original list prices.

How They Made It Happen

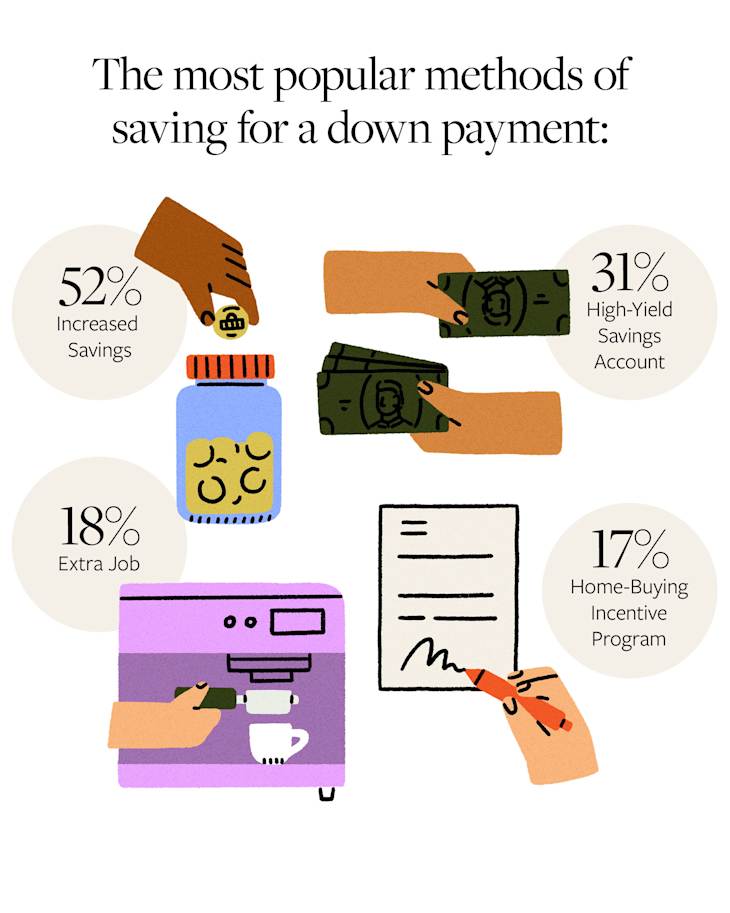

The idea of coming up with a down payment can be hard to wrap your brain around. Most respondents (52 percent) started by contributing more to their savings accounts. Thirty-one percent also opened high-yield savings accounts, which is a great way to put your money to work! Some buyers got closer to their goals by working extra jobs (18 percent) or taking advantage of home-buying incentive programs (17 percent).

In addition to saving, some prospective buyers also reported being open to non-traditional buying methods like renting-to-own (33 percent), becoming a landlord (29 percent) or buying a tiny home (28 percent). Out of those surveyed, 1 in 5 homebuyers received or will receive monetary help, which will most likely come from parents (82 percent).

The Other Costs That Surprised Them

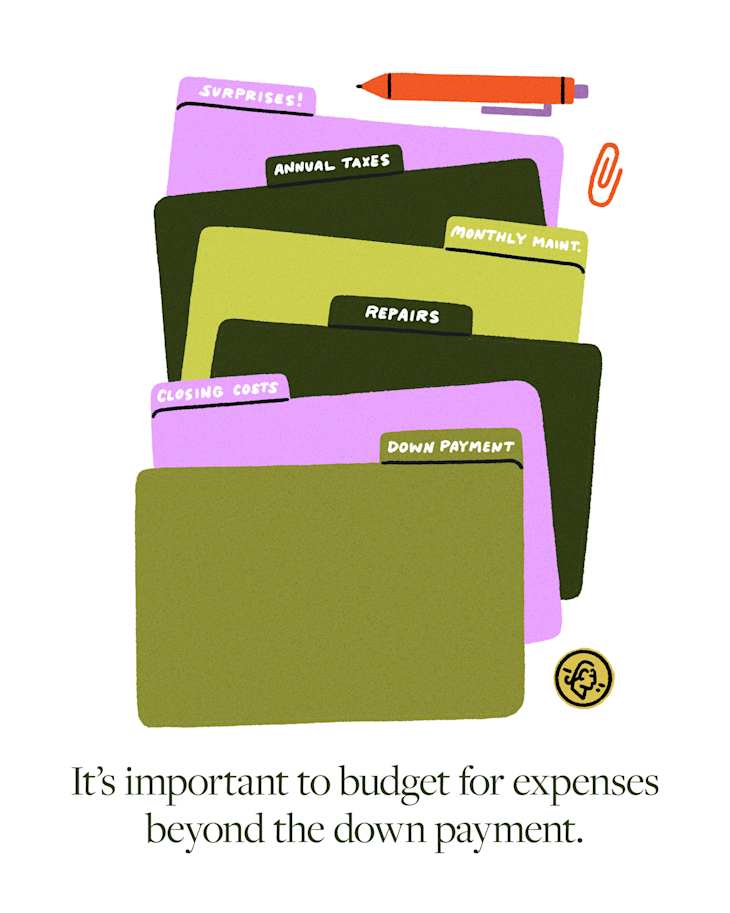

We also asked readers to tell us about the financial moves that they didn’t see coming — and they delivered some hard-earned insights! Additional expenses pop up during the home-buying process, like inspections, title fees, and transfer taxes. Another caution that came up again and again was remodeling. Respondents said they wished they’d known how much it would cost to make updates. “I wish I’d known how expensive plumbing is,” one said. “I thought we would be able to remodel our bathrooms completely but we can’t afford to.” Another respondent said it might even be worthwhile to put less money down, freeing up more cash for repairs. “Your mortgage interest rate will most likely be less than the credit card you end up using,” they said. (Always discuss your personal financial situation with trusted advisors.)