Reality Check: Nearly $1 Trillion Worth of Homes at Risk from Rising Sea Levels

Last month was the fifth anniversary of Superstorm Sandy’s deadly, destructive rampage through New York and New Jersey, which killed 157 people and left $50 billion in damage in its wake. Unfortunately, New York City is still unprepared for an increasingly likely flood disaster, and it’s among the U.S. cities most at risk from rising sea levels in the coming decades.

A new analysis by Zillow found that nearly 2 million U.S. homes worth close to $1 trillion would be lost if sea levels rose by an average of six feet. Now, waters won’t rise uniformly, and there’s no guarantee they will rise that much or very soon. But it’s a realistic end-of-century estimate if little to no action is taken to reduce emissions. (A 2015 study estimated that total emissions to date are already enough to lock in about 5 feet of sea level rise in due time.)

Ground zero for this threat is Miami, where almost a quarter (24.2%) of all homes could be underwater by the end of this century. More than 37,000 homes in Miami Beach alone — a full 78% of the neighborhood, worth $33 billion — would be underwater if sea levels rose six feet.

In fact, five of the ten U.S. cities with the most at-risk homes (and eight of the top 20) are in Florida. Between them, nearly a million Florida residences valued at more than $380 billion are in danger of being somewhat submerged by 2100.

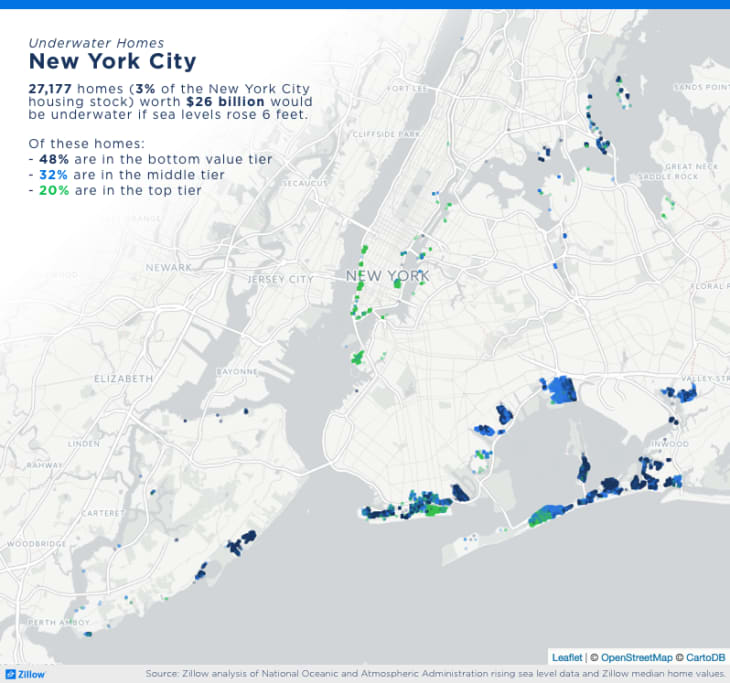

But it’s not just Florida’s problem. New York City has 180,267 homes — or $123.2 billion worth — at risk, according to Zillow’s analysis; in Boston, 52,694 homes valued at $42.7 billion are threatened by higher sea levels. And more than half (56.6%) of all homes in Upper Township, N.J., would be in the water given a six-foot sea level rise, for a waterlogged loss of $29.3 billion.

The Zillow report illustrates that while much of the projected property losses would hit the pricey downtown waterfront condos and beachside vacation houses you’d expect, rising sea levels would wreak a lot of devastation on average homeowners as well: Two thirds of the at-risk homes are in the suburbs, and 61% are valued at the median price for their area or below.

That’s troublesome for a couple of different reasons. For one thing, low- and middle-income homeowners have far more of their wealth tied up in their homes than the wealthy, who generally own more stocks and other investments. And residents in expensive cities may benefit from state, federal, or municipal mitigation efforts, such as the various seawalls and storm barriers being proposed for New York‘s and Boston‘s harbors.

In 2016, Freddie Mac chief economist Sean Becketti warned that climate change could present an even bigger threat to the economy than the housing crisis. Since most Americans’ wealth is locked up in their home equity, he reasoned, “If those homes become uninsurable and unmarketable, the values of the homes will plummet, perhaps to zero. Unlike the [housing crisis], homeowners will have no expectation that the values of their homes will ever recover.” With no point in rebuilding and businesses forced to relocate, he said, whole communities may vanish or unravel, and it will be difficult to pin down the timing of such an event — whether values will deflate gradually as the ocean encroaches, or plunge the first time a nearby home is deemed uninsurable.

That’s pretty dire stuff. And yet, it hasn’t stopped people from buying up coastal or low-lying properties with increasing abandon. What could change that, Redfin chief economist Nela Richardson told me, is a series of destructive storms. “But we’ve seen it with Hurricane Sandy and other really devastating storms, that after a few years the developers come back and build in those same risky areas,” she said.

One reason for that is the National Flood Insurance Program. A recent episode of “Last Week Tonight with John Oliver” dove into the wet workings of the federal flood insurance program, which in effect subsidizes homeowners who buy in flood-prone areas.

Now, flood insurance is pretty expensive, but it’s not nearly as expensive as it probably should be, given the risk for catastrophic damage: 90% of FEMA’s disaster claims are flood-related.

The program was well intentioned, designed to protect homeowners in coastal or riverfront areas from losing everything since private insurance wouldn’t cover them. But studies have shown that subsidized flood insurance encourages people to live and build in high-risk areas at the expense of other taxpayers.

“Historically, there wasn’t a huge building boom on Cape Cod until flood insurance was introduced,” said Peter MacDonald, co-owner and risk advisor at Murray and MacDonald Insurance in Falmouth, Mass. “Before [that], you couldn’t really build unless you were paying cash, it was too risky. But once you had flood insurance, the banks would say, ‘Yeah, we can lend you money.'”

The program has also been insolvent for years, paying out more than it takes in. A 2012 attempt by Congress to better align flood insurance rates with the underlying risks met with fierce backlash; much of the law was repealed a year later. “People living in floodplains haven’t really been paying the full cost of the flood risk,” said Ellen Douglas, associate professor of hydrology at University of Massachusetts Boston. “And when insurance companies then have to increase premiums to reflect the full cost of risk, it can be quite a shock — often more than homeowners in these areas can afford. It’s a real conundrum.”

Richardson sees a moral hazard in the subsidies. “There’s kind of an incentive problem. If homebuyers and cities and local governments had to completely internalize the actual risks, they might make different choices,” she said. “But as long as government is kind of backing them up, they’re less likely to incorporate the risk of climate change into their home buying decisions.”