Struggling to Save for a Down Payment? This Might be the Reason

If you’ve ever written a monthly check to Sallie Mae, the findings of a new study on student loan debt and millennial homeownership shouldn’t surprise you: College graduates with loan debt have a harder time saving up for a down payment than those who graduate debt-free.

That’s according to a study released Thursday by rental website Apartment List. Maybe we didn’t need a whole fancy study to innately grasp this perfectly obvious economic concept — but now that we’ve got one, there are a few interesting data bits to look at.

Student Debt & Down Payments, by the Numbers

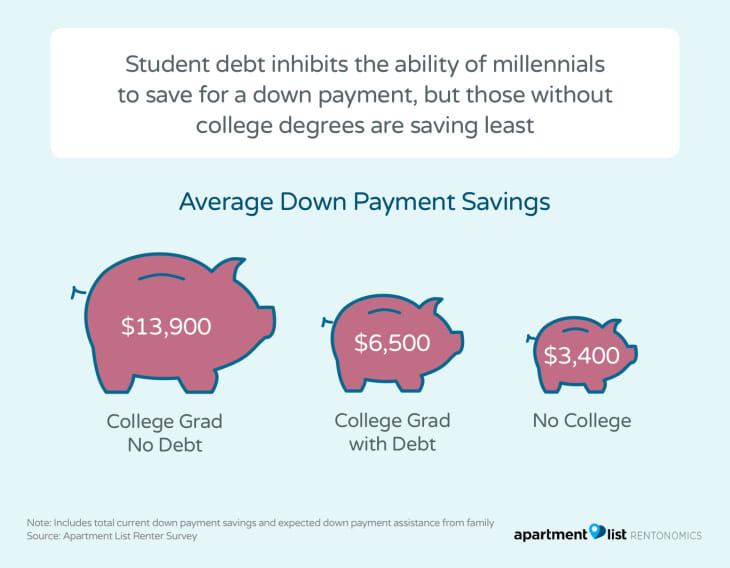

Millennial college graduates without debt have more than twice as much money saved up for a down payment as those with debt: $10,370 on average, compared to $4,320. But the debt-free grads also expect more help from family members ($3,570 vs. $2,220) when it comes time to buy a house. That makes sense — students who don’t need loans for school are more likely to come from affluent families who can help them out.

And while student debt takes its toll, the study confirms what we already know: a college degree still generally pays off (and makes it more likely you’ll own a home), despite the ridiculous price tag. Millennials without a college degree fare even worse than those with student loan debt, with just $2,240 saved up toward a down payment and an average family contribution of $1,130.

College grads without debt are able to save $300 a month toward a down payment, compared to $240 among those with loans and $180 for those with no degree. (It’s unclear how many without a degree do, in fact, have some residual student loans; debt without a degree to show for it is the worst possible combination, and could be dramatically hindering their savings.)

How Long Does it Take to Save for a Down Payment with Student Loan Debt?

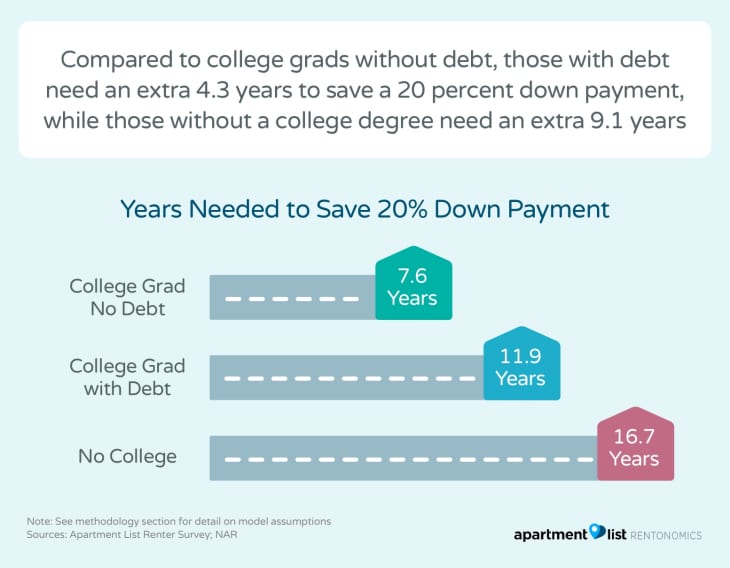

The study found that four out of five millennials — steady across all three groups — want to buy a home someday. But millennial college graduates without student loan debt are years ahead of their peers when it comes to saving up a down payment.

At a national level, Apartment List calculates it would take a debt-free college grad 7.6 years to save up a 20% down payment on a median-priced $222,000 condo, compared to 11.9 years for a grad with student loan debt. And millennials without a degree can expect it to take more than twice as long: 16.7 years. (Keep in mind, though, that the average down payment for buyers under 35 is actually more like 8%.)

Of course, these numbers are national averages, and they tend to go haywire in specific cities.

In San Francisco, debt-free grads need 12.4 years to save up a 20% down payment, but it will take an indebted graduate more than 27 years to reach that milestone, by which point a condo in the Mission will likely cost $4 trillion. Even Bay Area millennials with no college degree will hit their down payment sooner, in 24.2 years.

In Miami, Minneapolis, and Philadelphia, meanwhile, even graduates with debt can expect to save up a down payment in eight years or less.

And in Boston, remarkably, college graduates with debt are saving faster — just barely, but faster nonetheless — than those without any loan debt. An indebted college graduate will save up a down payment in 14.3 years there, compared to 14.8 for a debt-free graduate.

The same is true in Austin, Texas — where indebted grads (13.4 years) are more than a year ahead of their debt-free counterparts (14.7 years) — and in Charlotte, N.C., too. I’m not sure that’s good news so much as that prices are so crazy high, everybody’s screwed. Or perhaps private universities and advanced degrees (and the increased debt burdens each tends to create) are simply better rewarded in the economies of these outliers.

What Does this Mean for the Housing Market?

Studies confirm that all that student debt — $1.4 trillion of it, according to a 2017 report by American Student Assistance — is a drag on young home buyers. Among millennial student loan borrowers who don’t own a home, 83% say their student loan debt has delayed their decision to buy a home. And not by a couple months — by an average of seven years.

If a lot of millennials — now the largest generation of Americans — are locked out of the housing market for almost a decade longer than necessary, that can have all kinds of cascading effects. With their repeated trips to Home Depot and IKEA, first-time home buyers are a huge part of the economy, and they allow existing homeowners to trade up as their families or incomes grow.

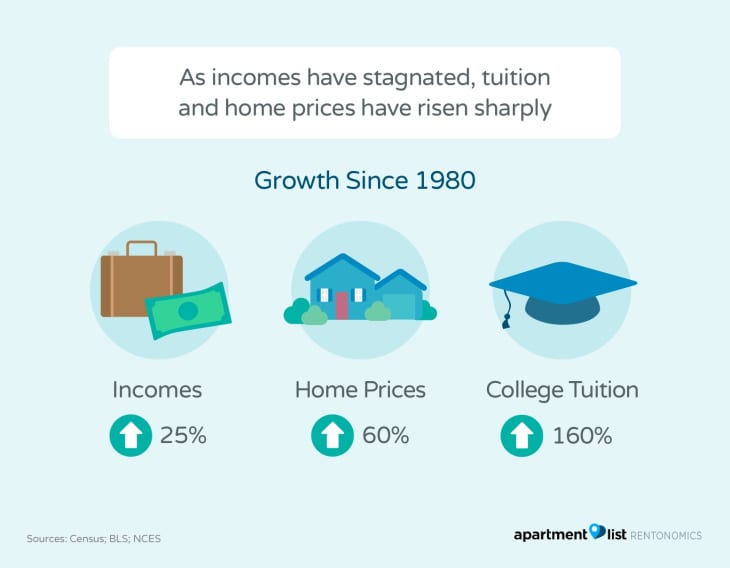

One last tidbit in the Apartment List study: While household incomes have increased 25% since 1980 (adjusted for inflation), home prices have risen 60%. So regardless of student loans, it’s already twice as hard to afford a home. But college tuition has skyrocketed 160% in that time.

While Americans increasingly need a college degree to afford a home, way more students now need loans to cover the cost of that degree. This kind of math gets ugly, and the vicious spiral is already ensnaring a generation of hopeful homebuyers.