Use These Checklists If You’re Planning to Buy a House in 3 Years, 1 Year, Or 3 Months

You’ve got your mind set on buying a home. Maybe you’re playing a long game, slowly but steadily building up that “down payment” savings fund. Or perhaps you’re hoping to be moved in and settled by the start of the new year. Wherever you are in your homebuying journey, experts say there are a number of steps you can take to gain solid financial footing and make the whole process a bit more seamless.

Consider this your homebuying roadmap, no matter if you’re aspiring to purchase your very own home in three years, one year, or three months.

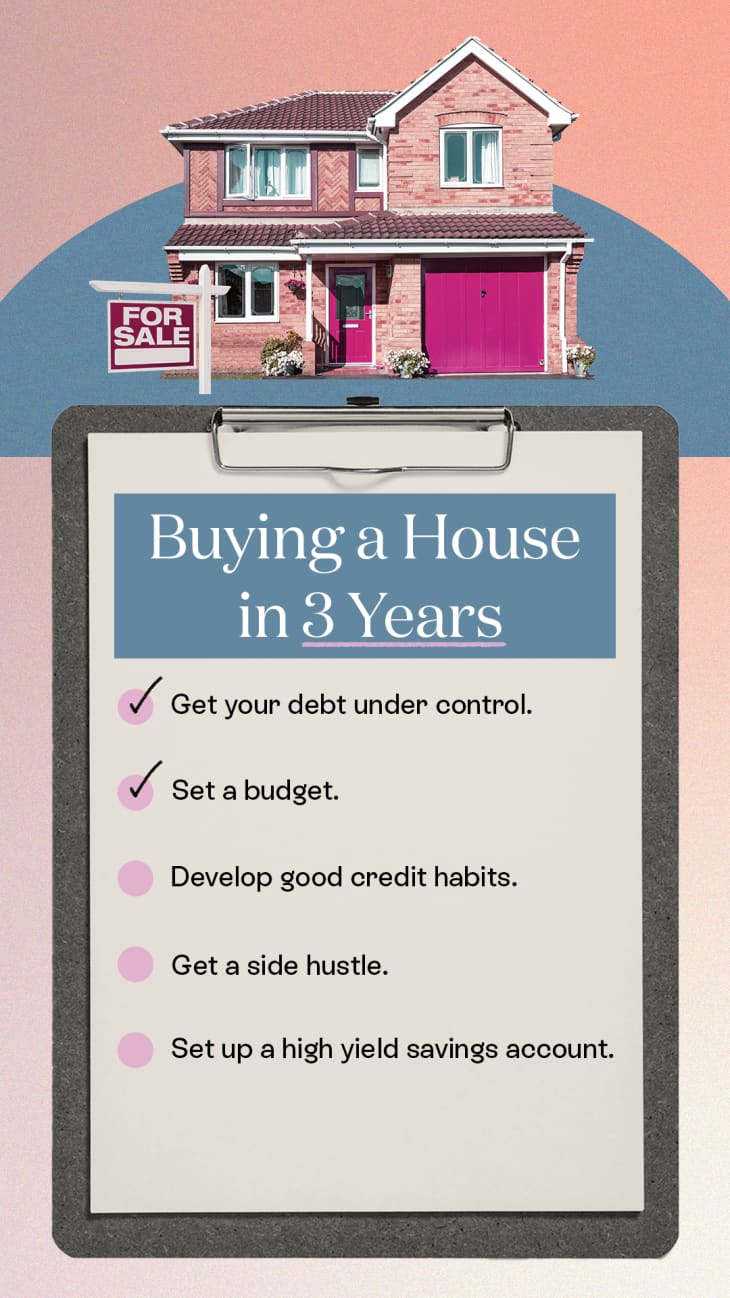

If You’re Planning to Buy in 3 Years…

If you’re eyeing homeownership in the next few years, now is a great time to rein in any outstanding debt and start saving for a down payment. You’ve got a few years to get your financial situation in tip-top shape so use this time to build your financial fitness.

1. Get your debt under control.

Not only does carrying a debt load make it more difficult to save for a house, but it can also make it more difficult to qualify for a mortgage, says Andy Taylor, general manager of Credit Karma Home. Lenders take into account how much of your income is going towards paying debts, which is known as your debt-to-income ratio (DTI). Most lenders look for a DTI that is less than 43 percent.

“Your DTI is an important factor because it shows a lender that you won’t be using up all of your remaining cash on making your house payment,” he says. While you may not be able to pay off your entire car loan or your student loans in the next few years, you can reduce the balances and pay down your revolving debt, like those credit card balances. Not sure where to start? Try downloading a money-saving app like Digit, which rounds up dollars and cents on your payments and adds them to a savings account. Then, you can use this extra cash to chip away at your credit card balances.

2. Set a budget.

Home prices, interest rates and, most likely, your own salary, will fluctuate over the next three years. But it’s smart to get a snapshot of how much you’ll be saving for a down payment and closing costs, says finance and savings expert Andrea Woroch. This way, you can start stashing away money with a goal in mind. Woroch recommends using online mortgage calculators to help you figure out how much you can afford on living expenses, layering in factors like taxes and HOA dues.

You may have heard that 20 percent is a gold standard for a down payment, but that’s a bit of a myth these days. While a larger down payment will help you avoid costs like private mortgage insurance, the minimum down payment for an FHA loan is just 3.5 percent, and conventional loans require as little as 3 to 5 percent down. (Here are the pros and cons of lower down payments). Closing costs, meanwhile, tend to be 2 to 5 percent of a home’s sale price, so remember to add a cushion to your budget to account for them.

3. Develop good credit habits.

Not only will excellent credit help you qualify for a mortgage, it will also help you nab a competitive interest rate. For most conventional loans, you’ll need a credit score of at least 620. You’ll get the best interest rates with a credit score of 760 or above. Paying all of your current bills on time will help build (or solidify) a healthy credit score, says Ron Wysocarski, a real estate broker based in Port Orange, Florida. Thirty-five percent of your credit score is based on your payment history. Some other good credit habits to establish include keeping your credit card utilization under 30 percent and checking your credit report regularly, disputing any errors.

4. Get a side hustle.

With a few years to go before you want to buy your home, think about how you can increase your down payment savings and fast track your debt repayment, Woroch suggests. “There are plenty of flexible side hustles you can do from home and in your spare time even if you feel limited with your current schedule,” Woroch says. For instance, you can sign up as a tutor through VarsityTutors.com and help students for an hour here or there in the subject of your speciality via Zoom, or make extra money by pet sitting via sites like Rover.com. Here are more ideas for side hustles to help you increase your income.

5. Set up a high yield savings account.

Open up a specific high yield savings account for your home fund, says Brittney Castro, a certified financial planner with Mint. Since your goal is to purchase a home within three years, you don’t want to take on too much risk with your money by investing it, she says. It’s smart to reduce risk and accept the lower rate of return you get from a high yield savings account to ensure your principal will be there when it comes time to buy. To make sure you stay on track with your savings goals, you can set up automatic transfers.

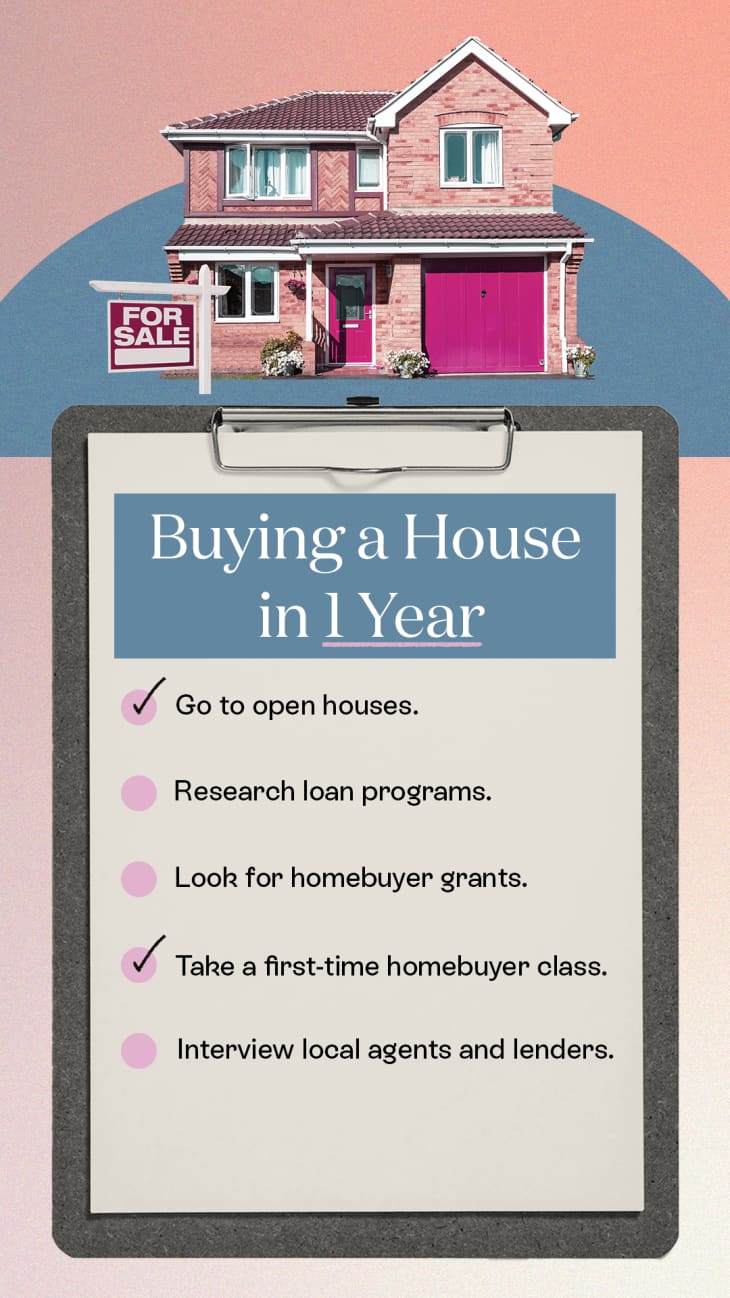

If You’re Planning to Buy in 1 Year…

In addition to keeping your credit score in good shape and paying off existing debt, you can spend the next year learning about the homebuying process, which will grow your confidence and position you as a savvy buyer.

1. Go to open houses.

Hit the open house circuit! This is a low-commitment way of scoping out what the market is looking like and you can get an idea of the type of home you’d like to purchase, says Jennifer Gale, a real estate agent in Ontario, Canada. As you start to zero in on which features are important to you and what neighborhoods appeal to you, you’ll get to see what homes in your price range look like. Plus, you’ll meet some potential real estate agents, Gale says.

2. Research loan programs.

Now is the perfect time to get a solid understanding of the different types of loans that are available and start considering which ones might be a best fit for you, says Brandi Wright, a strategic real estate advisor at Real Estate Bees in Denver, Colorado.

For instance, Federal Housing Administration, or FHA, loans are popular among first-time homebuyers because of their lower credit score requirements. With FHA loans, you can have a score as low as 500 so long as you bring a 10 percent down payment to the closing table. Conventional loans (i.e. loans that aren’t federally backed) typically require a credit score of 620 or higher.

Beyond loan types, you’ll also want to get familiar with loan terms. Fixed-rate loans lock you into an interest rate for the duration of your loan (ah, predictability!) while adjustable-rate loans, which have fallen out of favor while interest rates are at record lows, offer low, introductory rates and then are subject to adjust on an annual basis. You’ll also need to decide if you want to take on a 30-year mortgage with lower monthly payments or a 15-year mortgage that’ll save you on interest over the life of your loan.

“Knowing which loan products work for you will help you interview loan officers and it’s extremely important to know that not all lenders are able to offer the same loan products, or they could be inexperienced with the loan product you are interested in,” Wright says.

3. Look for homebuyer grants.

Not only should you get familiar with loan products, but it’s a savvy move to start researching first-time homebuyer programs and down payment assistance programs, Wright suggests.

There are more than 2,500 down payment assistance programs available, according to The Mortgage Reports. Some are from non-profit organizations, but the majority of them come from state and area housing finance agencies. Most of these programs are aimed at helping first-time buyers, but if it’s been a few years since you’ve last owned a home, you may qualify.

4. Take a first-time homebuyer class.

When you’re starting to get serious about shopping for a home, taking a first-time homebuyer class can help arm you with some confidence. Topics covered include things like understanding your credit score and reports, how to get a mortgage, how to close on a mortgage loan, and how to avoid defaulting on your loan.

Classes typically cost under $200, though many are free. Here are four helpful courses for first-time buyers.

5. Interview local agents and lenders.

Assembling a savvy team of real estate professionals is especially important in this unprecedented market. While it’s nice to hire your friend or a former classmate, remember that buying a home is likely the biggest financial decision of your life, Wright says. With that in mind, you should look to hire an agent or lender who has a proven track record in your market and is knowledgeable and passionate, she says.

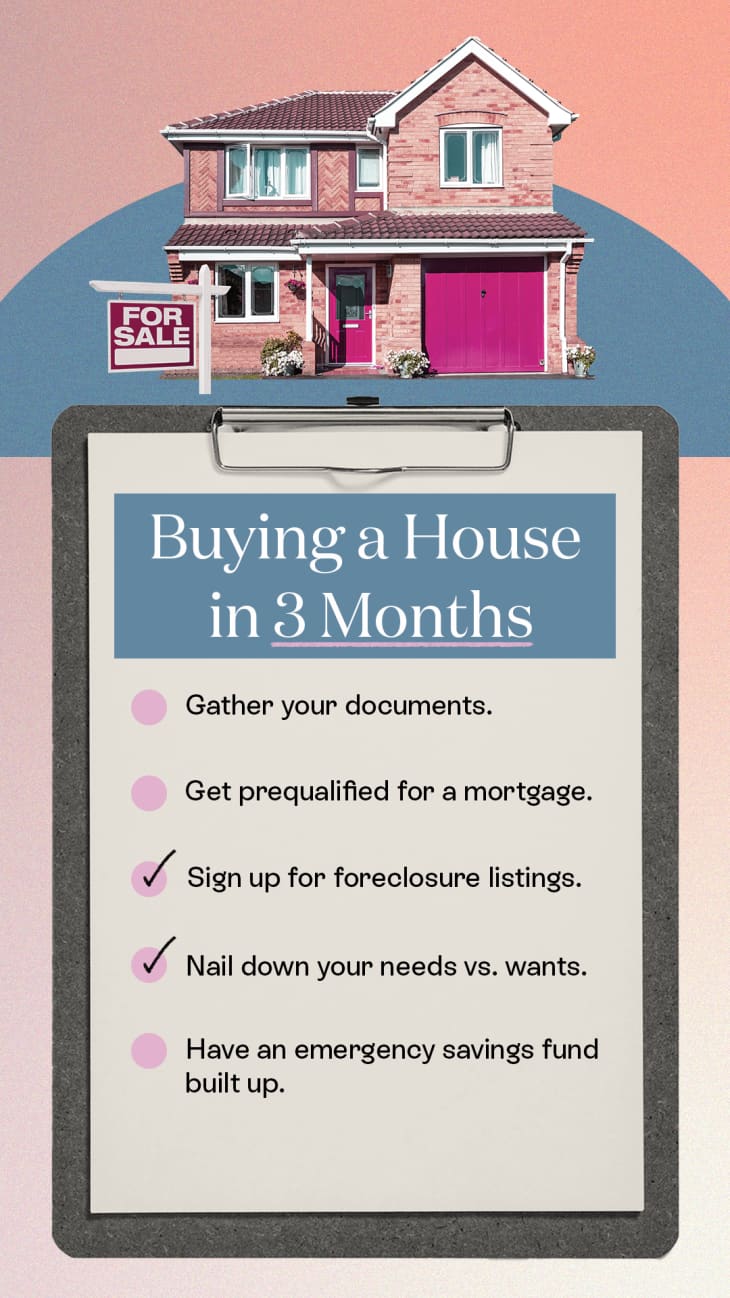

If You’re Planning to Buy in 3 Months…

During these next few months, you want to keep your financial situation stable. This means you shouldn’t take out a new car loan or max out your credit card, because it could jeopardize your ability to close on a mortgage. Ahead, find a few more homebuying tips for the home stretch.

1. Gather your documents.

The mortgage application process requires a lot of documentation, and requests for things like bank statements or tax returns will come at you quickly. To help expedite this process, put together a binder of important documents, suggests Alex Leduc, principal mortgage broker at Perch, a Canadian digital homebuying platform. Here are a few of his suggestions:

- Update any expired government-issued photo IDs that may be required by lenders.

- Download and organize financial statements and have them ready to be sent via email or uploaded to a secure website. This includes bank statements, tax returns, and employment letters.

- Stay liquid. If you have any investments that you’re planning to use in your down payment and that are in a fluctuating asset class (ex: cryptocurrency, stocks, etc.) liquidate them and move it into a high interest savings account. If you had 20 percent down payment ready, and then your bitcoin suddenly loses 30 percent of its value in a week, you wouldn’t want to be stuck with insufficient funds a week before your closing date.

- Move your money into an accessible bank account with physical branches. Some online-only, digital banks can take up to a week to issue a bank draft, whereas bank branches can issue them instantly. This is important when you have an accepted offer and need to get the deposit paid in 24 hours.

Also, if a family member or a friend is giving you a financial gift to help shore up your down payment, you’ll want to have a gift letter on hand that states the money is, indeed, a gift. Lenders want to ensure the money isn’t an informal loan that you’ll need to pay back, potentially putting pressure on your budget.

2. Get prequalified for a mortgage.

Now is the time to get prequalified for a home mortgage loan, says Brittney Castro, a certified financial planner with Mint. Mortgage rate locks typically last from 30 to 60 days, though some can last to 120 days or more, she says.

“It’s important to check with your lender as some will offer a free rate lock for a specified period,” Castro says.

3. Sign up for foreclosure listings.

Because of the inventory shortage, some first-time buyers are having luck finding homes before they hit the market. Foreclosures may not pop up on typical listings sites, but you can sign up for these through special feeds, Woroch says. You can find a list of sites to track foreclosures here, Woroch says. A real estate agent can also set up a foreclosure home alert that sends you emails directly about new properties available that meet your criteria.

“In the end, you may be able to get a deal on a foreclosure, put the money into making upgrades and still end up spending less than if you bought a brand new or recently renovated home,” she says.

4. Nail down your needs vs. wants.

There’s an informal rule in real estate that if a home checks off 85 percent of what you’re looking for in a property, you should put in an offer. It also helps to determine your needs vs. wants when looking for properties. For instance, if you and a partner are remote workers, a home office may be a top priority. But don’t rule out an otherwise great home because it doesn’t have, say, granite countertops, Bridges says.

5. Have an emergency savings fund built up.

You don’t want to wipe out your savings account when buying a house, cautions Ralph DiBugnara, president of Home Qualified, a real estate resource site. No matter how much you plan, there will likely be unforeseen expenses that pop up, he says. Many people will buy a home and then use credit cards to buy furniture, but those interest rates can be up to 10 times as much as a mortgage interest rate, he cautions.

Bookmark these checklists for your homebuying journey — and happy house-hunting!