Mortgage Rates Are Rising, Ready to Quietly Crush Your Homebuying Dreams

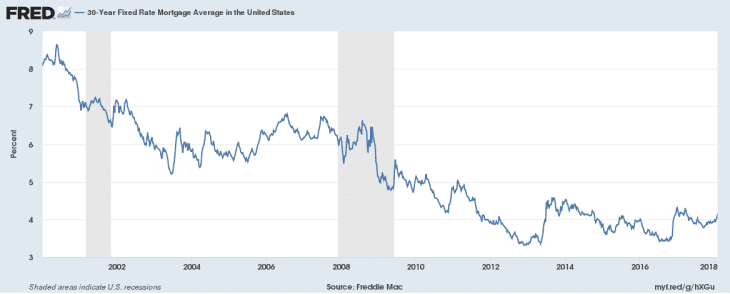

The average interest rate on a 30-year fixed-rate mortgage has surged past 4.28% this week to its highest point in years, according to CNBC. That’s bad news for home buyers, because even a small rate increase can be enough to push an already difficult-to-afford house completely out of reach.

After starting the year around 4.0%, average rates have been steadily creeping higher, with some lenders quoting best rates of 4.5% this week. That’s still low in the grand scheme of things, but Matthew Graham, chief operating officer of Mortgage News Daily, said rates look likely to keep climbing and advised homebuyers to get a rate lock sooner rather than later. “Lock early and plan on rates moving higher until we see a broad shift in momentum,” he wrote Monday.

It’s almost hard to wrap your head around it, but mortgage rates won’t always stay this low. We’ve grown accustomed to historically low interest rates in the wake of the Great Recession — it’s been a decade since the average rate on a 30-year mortgage cracked 6%, and a full seven years since we’ve seen 5%.

But while rates have crept up from their 40-year lows in the past couple of years, we’ve still been bouncing along near the bottom. And with nowhere for rates to go but up, economists have been predicting a gradual increase for years.

Mortgage rates of 5% to 7% were the norm throughout the early 2000s, while back in 1981, when my parents bought the house I grew up in, their mortgage came with a staggering 18% interest rate —akin to what credit cards charge today.

While no one expects a return of stagflation-era interest rates anytime soon, even a modest one-percentage point increase to the average mortgage rate can wipe out a homebuyer’s purchasing power.

For example, take a $250,000 home as an example, roughly the median U.S. home price in December.

With a 20% down payment ($50,000) saved up, a home buyer finances the remaining $200,000 with a 30-year mortgage at 4.0%. Her mortgage payment (before taxes and insurance) comes to $955 a month.

If that interest rate goes up by just one percentage point, to 5.0%, her monthly mortgage would increase to $1,074 — an extra $119 every month, or roughly 12% higher. If she can’t afford to pay more than the $955 a month she was initially banking on, she now has to downgrade her housing search to homes priced in the $225,000 range.

Since many millennials are struggling to save up a full down payment, they tend to finance more of their purchase — meaning higher rates play an even bigger role.

For young homebuyers, the effect is amplified. Since many millennials are struggling to save up a full down payment when student loans and high rents consume so much of their income, they tend to finance more of their purchase — meaning higher rates play an even bigger role.

A similar homebuyer with just a 5% down payment saved up ($12,500) will need to finance $237,500 of that home. And at a 5.0% interest rate, she’ll be paying $1,275 per month — now an extra $320 a month for the same $250,000 house.

Finally, the dream-crushing power of creeping interest rates is even more exaggerated in high-priced housing markets. Imagine a couple who’s saved up a 10% down payment on a $500,000 home in Seattle or New York. They ran the numbers with a 4.0% interest rate last month, and realized they could just afford the $2,148 monthly payment.

If rates climb to 5.0%, that payment shoots up $268 a month, to $2,416. Assuming they were already near their limit, now they have to scale down their house hunt, and look at homes priced about $40,000 less.

There are a lot of compromises one can make to bridge that gap — looking at homes farther from work, in a worse school district, or with less space or an outdated kitchen. But, simply put, it sucks to feel like something so completely out of your control has such an outsized impact on the home you can afford.